2026-05-12

For property and casualty carriers and MGAs, the ability to respond quickly to market changes depends heavily on how fast you can update your rates. If every rate change requires a development ticket, a release cycle, and a regression test, your actuaries and product managers are always waiting — and your competitive window narrows.

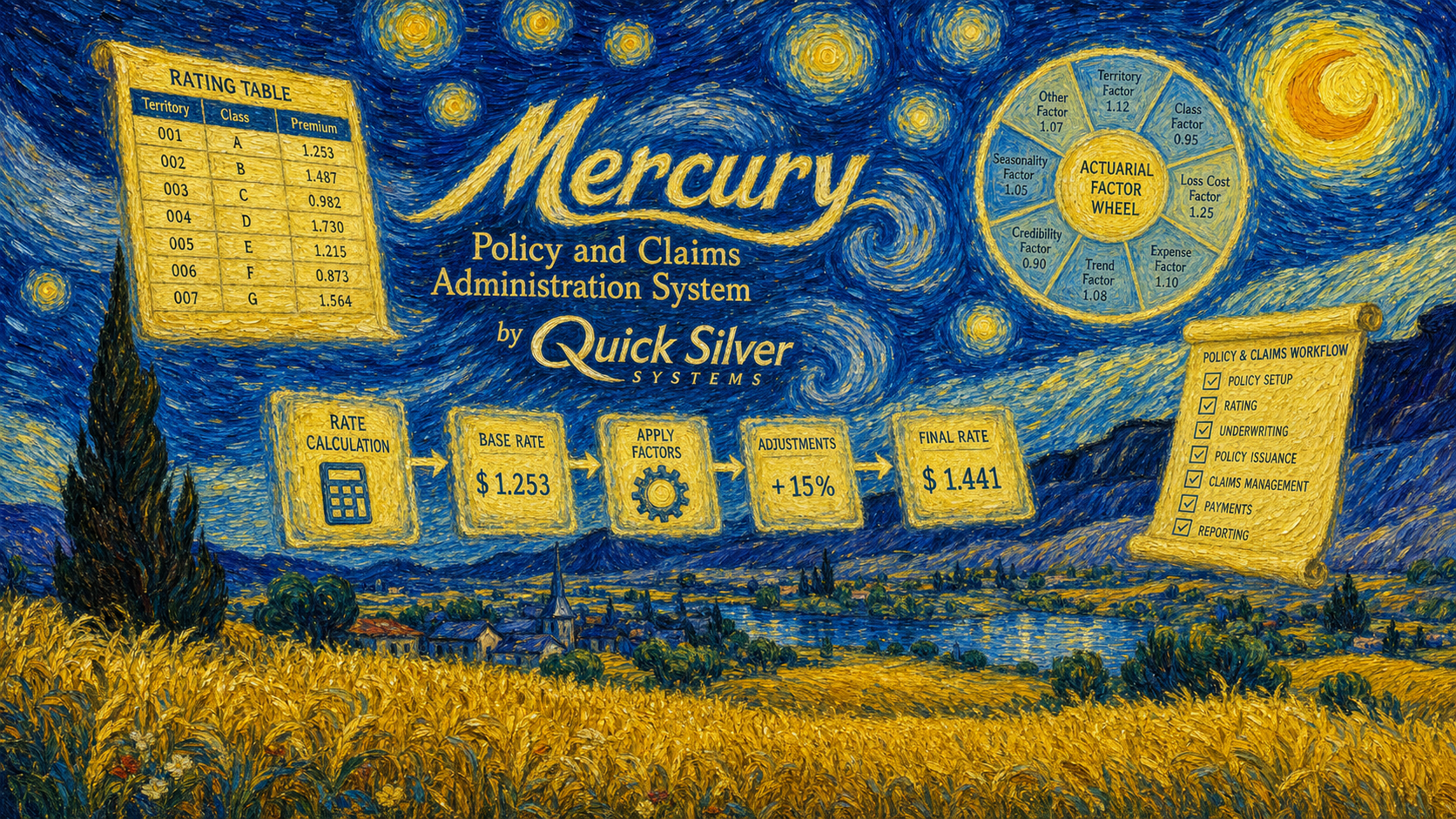

Mercury includes a configurable rating engine designed to give carriers and MGAs direct control over their rate tables, rating factors, and underwriting rules — without requiring code changes or vendor involvement for routine updates.

Insurance rating is complex. A single commercial auto policy might involve territory factors, vehicle class adjustments, driver experience credits, loss history surcharges, and multi-policy discounts — all multiplied across coverage types. Carriers need to update these parameters regularly in response to loss experience, regulatory filings, and competitive positioning.

When rating logic is locked in code, every change adds friction: development estimates, scheduling, testing, and deployment. Over time, this creates a backlog that makes actuarial responsiveness slow and increases the risk that live rates drift from filed rates.

A configurable rating engine solves this by separating the rate logic structure (which changes rarely) from the rate parameters (which change frequently). Business users — actuaries, product managers, underwriting operations — can update tables and factors through a governed admin workflow rather than submitting development requests.

In Mercury, rating configuration is built around the concept of editable rate tables and factor sequences rather than hard-coded formulas. This means:

For MGAs managing multiple carrier appointments, configurable rating is especially valuable. Each carrier relationship may have distinct rate structures, eligibility rules, and program parameters. A system that requires separate code deployments for each carrier's rate changes becomes a bottleneck quickly.

Mercury's design supports program-level rate configuration so that an MGA can maintain separate rating parameters for each carrier appointment within a single platform — without cross-contamination between programs.

Configurable rating is not the same as uncontrolled rating. Carriers and MGAs operating in regulated environments need to ensure that rate changes are approved, documented, and traceable to filed rates. A well-designed configurable rating system includes:

These controls ensure that configurability serves speed without creating compliance risk.

When rating configuration is in the hands of actuarial and product teams, carriers and MGAs can respond to loss trends and market opportunities faster. Rate accuracy improves because the feedback loop from loss experience to rate update shortens. And IT teams can focus on system improvements rather than routine rate maintenance.

For organizations considering a modern policy administration platform, rating configurability is one of the highest-leverage capabilities to evaluate — because it determines how fast you can operate and adapt once the system is live.

If your current rating process depends heavily on development resources for routine updates, Quick Silver Systems can help you assess what a configurable rating approach would look like for your book of business in Mercury.