Mercury AI-based data import supports carriers and MGAs load legacy policy, claims, and billing data faster, while validations that cut onboarding rework for carrier teams.

Read More...

Connect ISO/Verisk partner services to Mercury so underwriting and claims teams can validate risk inputs faster and keep work moving.

Read More...

A quick look at how Mercury helps insurance teams standardize steps and reduce friction with this capability.

Read More...

How Mercury IVR helps insurance teams route callers to the right workflow quickly, cutting transfers and accelerating service for carriers, MGAs, and TPAs.

Read More...

A quick look at how PCI-aligned payment collection can support secure, streamlined premium billing workflows in Mercury.

Read More...

A practical look at how digital refunds can reduce billing friction with clearer audit trails and faster reconciliation for insurance operations teams.

Read More...

Build role-based operational reports without manual spreadsheets, so insurance teams can monitor performance and act on exceptions faster.

Read More...

Use Mercury IVR to route policy and claim calls quickly, cutting transfers and speeding intake for carriers, MGAs, and TPAs while keeping service consistent.

Read More...

Mercury helps underwriting and claims teams use AI RAG search and NLP to quickly find policy and claim answers and reduce manual document hunting.

Read More...

See how Mercury supports digital payments with a workflow that helps insurance teams post accurately and reduce billing friction across programs.

Read More...

Highlight OFAC sanctions screening in Mercury billing and disbursements to reduce payment risk and keep carrier workflows moving.

Read More...

See how Mercury e-signatures help carriers and MGAs shorten binder-to-policy issuance while keeping status, tracking, and records connected to billing and service.

Read More...

PCI-compliant collection keeps billing secure while staying connected to policy workflows and operational controls for carriers, MGAs, and TPAs.

Read More...

See how carriers and MGAs can reduce conversion risk with AI-assisted mapping, validation, and exception handling for policy, billing, and claims data imports.

Read More...

A quick look at how Mercury helps insurance organizations configure workflows without code, so teams can adapt faster while keeping controls in place.

Read More...

Secure PCI-compliant payment collection helps carriers, MGAs, and TPAs reduce friction and keep billing workflows consistent end to end.

Read More...

See how Mercury supports online bill pay plus reminders that reduce service calls and improve premium collection for carriers and MGAs.

Read More...

Highlights how Mercury helps insurance teams update screens quickly, keeping policy and claims work consistent as products and rules change.

Read More...

See how Mercury helps carriers and MGAs automate underwriting letters with rules and reusable templates so decisions go out faster with less manual follow-up.

Read More...

Explore how Mercury SMS messaging supports automated reminders and claim status alerts to keep carrier and MGA communications timely and consistent.

Read More...

Speed First Notice of Loss intake with a self-service experience that captures consistent loss details and routes claims to the right team for carriers and MGAs.

Read More...

PCI-aligned payment collection in Mercury helps carriers, MGAs, and TPAs take card payments for billing and fees while reducing sensitive data exposure.

Read More...

Mercury helps carriers and MGAs connect portals, billing, and partner data through an API-first foundation that supports faster automation and fewer integration surprises.

Read More...

Mercury low-code configuration lets carriers, MGAs, and TPAs adjust workflows, screens, and rules through governed configuration instead of long IT cycles.

Read More...

Mercury helps carriers and MGAs deliver certificates of insurance on demand through a self-service portal, with governance controls and a clear audit trail.

Read More...

Mercury lets carriers, MGAs, and TPAs flag catastrophe claims directly inside the claims workflow, speeding triage and keeping reinsurance reporting clean.

Read More...

See how an accounting-based core supports audit-ready reconciliation for billing, commissions, and claims payment records across policy and claims operations.

Read More...

Use Mercury IVR routing to capture caller intent, reduce transfers, and move service and claims inquiries to the right workflow faster for carriers, MGAs, and TPAs.

Read More...

Integrate ISO/Verisk data into Mercury workflows to speed claims intake and reduce manual rekeying. Built for carriers, MGAs, and TPAs that need consistent downstream data.

Read More...

Mercury supports exclusionary filters during rate and quote so teams can stop ineligible risks earlier and keep underwriting decisions moving with less rework.

Read More...

Mercury supports self-service premium payments and automated reminders so insurance teams can reduce billing inquiries and improve on-time collections.

Read More...

How Mercury supports digital refunds for premium overpayments and claim reversals, with audit trails and operational controls for insurance teams.

Read More...

Mercury connects carriers, MGAs, and TPAs to ISO and Verisk data feeds so rating, underwriting, and claims teams keep workflows accurate and fast.

Read More...

A flexible screen builder helps carriers, MGAs, and TPAs tailor policy and claims experiences quickly without waiting on long development cycles.

Read More...

PCI-compliant payment collection helps carriers, MGAs, and TPAs take premium and fee payments securely while keeping billing steps consistent for operations.

Read More...

SMS messaging in Mercury keeps carriers, MGAs, and TPAs in touch with policyholders through renewal reminders, claim status updates, and payment alerts.

Read More...

OFAC checks embedded in Mercury workflows help insurers keep disbursements and refunds moving while maintaining compliance controls across teams.

Read More...

Digital e-signatures on policy and claims forms help carriers, MGAs, and TPAs accelerate issuance, endorsements, and sign-offs with a secure audit trail.

Read More...

Mercury connects policy, claims, documents, and payments through APIs so carriers, MGAs, and TPAs can cut rekeying and run with stronger controls.

Read More...

Configurable rating helps carriers, MGAs, and TPAs update pricing inputs quickly while keeping versions, approvals, and audit trails consistent across programs.

Read More...

See how Mercury helps carriers, MGAs, and TPAs standardize underwriting and claims workflows with configurable steps, clearer handoffs, and reliable controls.

Read More...

Mercury helps carriers, MGAs, and TPAs move claim funds faster using digital disbursements with stronger controls, fewer errors, and clearer audit support.

Read More...

API-first integrations help carriers, MGAs, and TPAs connect portals, billing, analytics, and partner data flows without heavy custom code.

Read More...

See how Mercury’s API-first integration hub helps P&C carriers, MGAs, and TPAs connect portals, billing, analytics, and data flows with less custom development.

Read More...

API-first connectivity helps carriers, MGAs, and TPAs link Mercury to portals, billing, and analytics so integrations scale without brittle point-to-point work.

Read More...

Mercury runs on AWS as a true cloud SaaS, giving carriers, MGAs, and TPAs scalable policy and claims administration without on-premise infrastructure costs.

Read More...

Mercury meets HIPAA security standards so carriers and TPAs managing health-adjacent lines can handle policies and claims data with consistent governance.

Read More...

Connect portals, billing, and payments through one integration layer. Mercury helps carriers, MGAs, and TPAs move data reliably without constant point-to-point rework.

Read More...

Mercury helps carriers, MGAs, and TPAs connect portals, billing, payments, and data feeds through API-first integrations designed to reduce brittle point solutions.

Read More...

Mercury enables carriers, MGAs, and TPAs to offer insureds a self-service portal for policy access, claims submission, and on-demand COI generation without staff intervention.

Read More...

See how Mercury helps carriers, MGAs, and TPAs connect portals, billing, and partner data through stable APIs to reduce brittle point-to-point work.

Read More...

For carriers, MGAs, and TPAs, Mercury helps streamline system connectivity with an API-first approach that supports cleaner data exchange across portals and partners.

Read More...

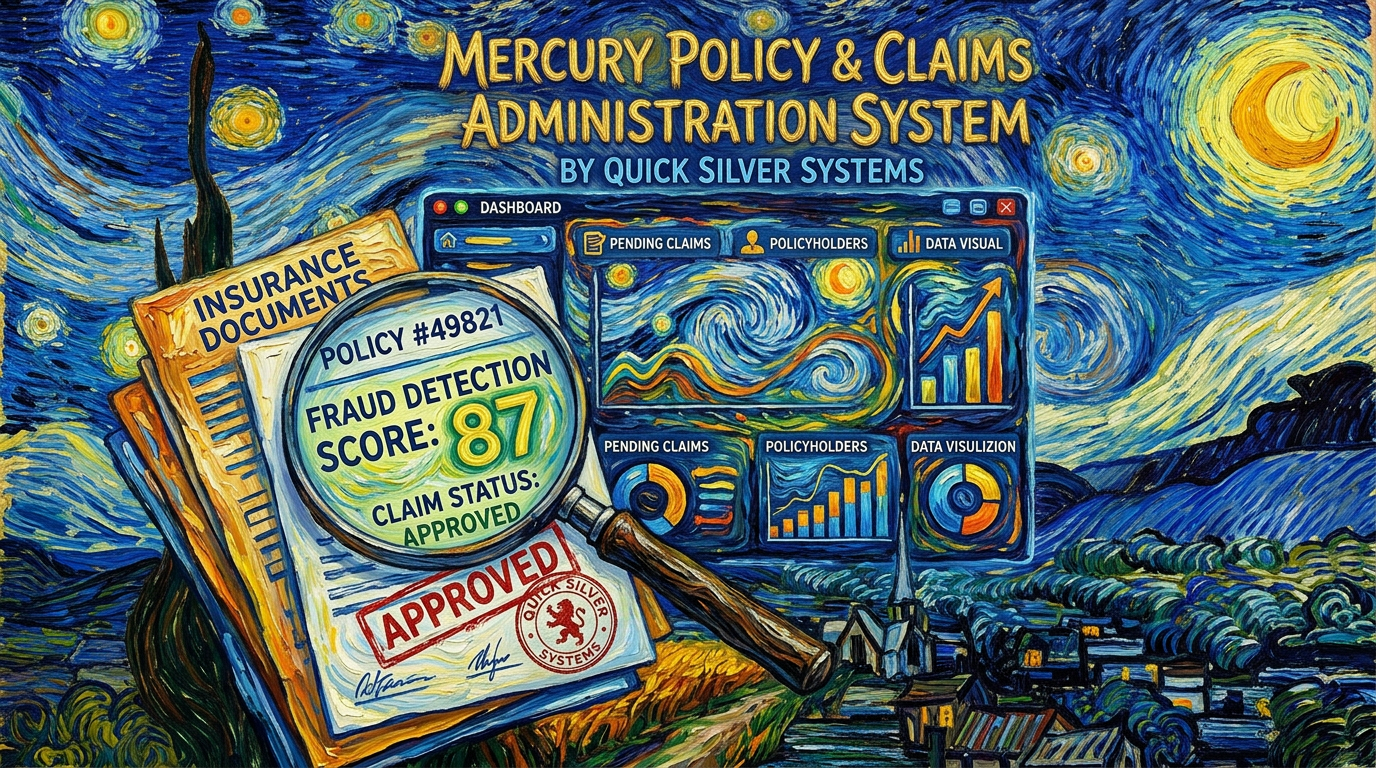

Mercury scores every claim document 1-100 for fraud risk using AI and NLP, giving carriers, MGAs, and TPAs a structured signal at first notice of loss.

Read More...

Mercury API-first design helps carriers, MGAs, and TPAs integrate portals, billing, data, and partners with governance.

Read More...

Mercury low-code configuration helps carriers, MGAs, and TPAs tailor underwriting and claims workflows without code.

Read More...

Mercury scores every claim document 1-100 for fraud risk using AI and NLP, giving carriers, MGAs, and TPAs a structured signal before adjudication.

Read More...

Driver-behavior telematics ingested directly into Mercury's policy and claims record -- one source of truth for underwriting, claims, and reinsurance teams.

Read More...

Mercury claims teams tag every affected loss to a named CAT event in one click -- reserves bucket correctly, reinsurance ceding flags are set, and the audit trail is intact.

Read More...

Mercury lets MGAs quote and bind across multiple carrier appetites from a single screen -- one submission, parallel rate plans, API-first data calls, full audit trail.

Read More...

Mercury's configurable rating engine treats filed rates as versioned, auditable data, not code -- carriers and MGAs can ship rate changes from a UI in days, not quarters.

Read More...

Insureds, producers, and claimants self-serve around the clock through Mercury portals -- including on-demand certificates of insurance -- against the same data the back office uses, with full audit trails.

Read More...

Every policy and every claim is a pile of documents. Mercury handles imaging, NLP extraction, and AI-powered fraud scoring natively, so carriers turn paperwork into structured data without a parallel toolchain.

Read More...

The submission-to-bind cycle is one of the clearest measures of core system performance -- Mercury was engineered to compress it through configurable workflow, rating, and API-integrated third-party data calls.

Read More...

Quick Silver Systems has designed Mercury to handle the multi-line complexity, compliance requirements, and integration needs that P&C carriers, MGAs, and TPAs require to compete effectively today.

Read More...

Leading chief claims officers are increasingly defined by their ability to build data infrastructure, analytics capability, and technology strategy -- not just claims expertise and operational management.

Read More...

Many P&C carriers systematically under-pursue subrogation opportunities, leaving recoveries on the table that would meaningfully improve loss ratios if captured consistently.

Read More...

A new generation of digitally sophisticated independent agents is growing market share by combining technology-enabled efficiency with the personal service that direct digital carriers cannot replicate.

Read More...

Growing regulatory scrutiny of environmental contamination, combined with expanded theories of liability in toxic tort litigation, is making environmental coverage a more complex underwriting challenge.

Read More...

Carriers that enrich new business submissions with third-party data at the point of quoting are writing risks they understand better from day one, with materially lower adverse selection rates.

Read More...

Expanding domestic logistics infrastructure, warehouse construction, and high-value cargo movements are driving premium growth opportunity in inland marine lines for carriers with the appetite.

Read More...

The carriers that emerge strongest from insurance market downturns are consistently those that avoided the temptation to chase premium volume at inadequate pricing during the preceding soft market period.

Read More...

Insurance billing platforms that support flexible payment schedules, automated reminders, and digital payment rails are reducing lapse rates and improving cash flow predictability for carriers.

Read More...

Rising construction volumes combined with labor shortages and materials substitution are elevating construction defect claim frequency and severity across general liability and builders risk lines.

Read More...

Policyholders compare their insurance experience to Amazon, Uber, and their bank -- not to other insurance carriers -- raising the bar for digital experience and speed across all interactions.

Read More...

Insurance carriers deploying machine learning models in claims fraud detection are identifying suspicious patterns earlier and with greater precision than traditional rule-based systems allow.

Read More...

As admitted homeowners markets retreat from high-risk coastal and wildfire-exposed territories, product designers are rethinking coverage structures, sublimits, and deductible frameworks to match real risk.

Read More...

Amid the complexity of modern insurance operations, disciplined loss reserve adequacy continues to be the most fundamental expression of a P&C carrier's financial health and operational credibility.

Read More...

Claims investigators are routinely incorporating social media review into personal injury files, and the evidence gathered is materially affecting outcomes in a significant portion of investigated cases.

Read More...

Insurance carriers with mature API ecosystems are launching new product lines in weeks rather than months by connecting configurable policy platforms with third-party data, distribution, and payment rails.

Read More...

The growing presence of third-party litigation funding in commercial liability cases is changing settlement dynamics and driving up average jury awards in ways that carriers must understand and address.

Read More...

The long-anticipated wave of experienced insurance professional retirements is accelerating, and carriers that have not built talent pipelines are feeling the knowledge transfer gap acutely.

Read More...

The excess and surplus lines market continues to absorb risks that admitted carriers are declining, with premium volume and carrier count both expanding in several casualty and property classes.

Read More...

With loss cost inflation persistent across multiple P&C lines, carriers are focusing intensely on expense ratio reduction as the controllable lever for combined ratio improvement.

Read More...

Self-service digital FNOL capabilities are now expected by a significant portion of claimants, particularly younger policyholders who prefer app or web-based claim initiation over phone intake.

Read More...

Research and industry experience increasingly support the view that diverse leadership teams make better decisions, particularly under the complex risk environments that insurers navigate.

Read More...

Insurance carriers that structure InsurTech partnerships around clearly defined business outcomes -- not technology capabilities -- report significantly better results and fewer abandoned implementations.

Read More...

Insurance carriers that piloted predictive underwriting analytics in recent years are now embedding those models directly into their core underwriting workflows rather than treating them as supplemental tools.

Read More...

Commercial property owners are confronting the realities of flood exposure more directly as both private market and NFIP coverage limitations become more apparent after recent loss events.

Read More...

Small commercial lines are seeing dramatic efficiency gains as straight-through processing reduces the manual touchpoints between submission and bound policy to near zero for qualifying risks.

Read More...

After years of declining claim frequency in workers compensation, some lines and geographies are seeing frequency stabilize or tick upward, prompting underwriters to revisit rate adequacy.

Read More...

Carriers and MGAs that have adopted API-first integration architectures are connecting with partners, data vendors, and distribution platforms at a speed that older EDI and batch models cannot match.

Read More...

Catastrophe modeling vendors are accelerating model update cycles as climate-influenced loss experience accumulates and exposes gaps in older probabilistic frameworks.

Read More...

Claims organizations that treat adjuster training as a strategic investment rather than an administrative expense are outperforming peers on both quality and customer satisfaction metrics.

Read More...

The availability and pricing of reinsurance capacity continue to have a direct and immediate effect on how primary P&C carriers position their portfolios and growth targets.

Read More...

Third-party administrators are under increasing pressure from self-insured clients and program carriers to deliver real-time claims data, clear performance metrics, and audit-ready reporting.

Read More...

Advanced analytics and AI tools in insurance deliver results only as good as the underlying data quality -- a lesson many carriers are learning the hard way.

Read More...

Parametric triggers are moving from catastrophe bonds and weather products into commercial lines and specialty coverages, opening new markets where traditional indemnity models struggle.

Read More...

Carriers and agents who engage policyholders consistently throughout the policy term report meaningfully higher retention rates than those who only reach out at renewal.

Read More...

Insurance technology buyers in 2026 expect cloud-native architecture as table stakes, not a differentiator, shifting vendor competition to configurability and integration depth.

Read More...

Small commercial carriers and MGAs are facing disproportionate regulatory compliance pressure as state requirements for data reporting and coverage mandates multiply.

Read More...

Managing General Agents have become a dominant force in specialty and niche P&C markets, combining underwriting expertise with distribution agility that traditional carriers often struggle to match.

Read More...

Usage-based and behavior-based telematics programs are enabling personal auto carriers to segment risk with a precision that traditional rating factors cannot match.

Read More...

While the industry debates AI and embedded insurance, the foundational challenge for many carriers remains the policy administration and claims systems built decades ago.

Read More...

After steep rate increases and coverage restrictions through 2023 to 2025, the cyber insurance market is beginning to stabilize as underwriting frameworks mature.

Read More...

Artificial intelligence is accelerating FNOL workflows, helping carriers acknowledge, route, and initiate claims faster than traditional intake processes allow.

Read More...

Claims leakage remains one of the largest controllable cost drivers in property and casualty insurance, yet many carriers still lack the tools to measure it precisely.

Read More...

After years of soft market conditions, underwriting discipline is reasserting itself across commercial P&C lines as loss costs and reinsurance pricing stabilize.

Read More...

Embedded insurance is no longer a novelty — it is becoming a primary channel for P&C carriers looking to reach customers at the point of need.

Read More...

The carriers that will lead the P&C insurance market in the mid-2030s are making foundational decisions today. Long-term thinking on technology, talent, and product design creates advantages that are difficult to replicate quickly.

Read More...

Conversational AI tools -- chatbots, voice assistants, and large language model-powered interfaces -- are changing how insurers handle routine customer interactions. The key is deploying them where they add value without degrading complex service moments.

Read More...

Loss reserve adequacy has become more challenging as social inflation, medical cost trends, and catastrophe frequency create wider uncertainty bands. Carriers that adapt their reserving practices are better positioned for volatility.

Read More...

Insurance plays an essential but often misunderstood role in disaster recovery. The speed and adequacy of claims payments have a measurable impact on how quickly communities rebuild and recover economically.

Read More...

Geospatial data -- satellite imagery, aerial photography, and parcel-level property data -- is transforming property underwriting. Carriers that use it well are making faster, more accurate risk decisions.

Read More...

The most successful insurance product innovations in recent years have started with structured policyholder feedback. Carriers that systematically collect and act on customer insight create products that win on value, not just price.

Read More...

Open banking data -- with policyholder consent -- is creating new opportunities for insurance product innovation, underwriting refinement, and customer engagement. Carriers should understand what is now possible.

Read More...

Subrogation recovery is one of the most consistently underinvested areas of claims operations. Carriers that build systematic, technology-enabled subrogation programs generate meaningful underwriting income that directly improves combined ratios.

Read More...

Insurance distribution is not moving entirely to direct digital -- it is becoming more omnichannel. Carriers that design for multiple channel preferences will reach broader markets without sacrificing service quality.

Read More...

Insurance AI governance is moving from voluntary best practice to regulatory expectation. Carriers that build accountability frameworks proactively will be better positioned when formal requirements arrive.

Read More...

Property claims severity has increased across homeowners and commercial property lines. Carriers that proactively manage vendor relationships, estimating tools, and subrogation programs are containing the impact.

Read More...

Claims excellence used to mean accurate, timely payment. In a digital-first environment, it also means transparent communication, self-service capability, and a frictionless policyholder experience throughout the lifecycle.

Read More...

Specialty lines MGAs are among the most innovative segments of the insurance market. Their technology choices -- particularly around underwriting workflow and data integration -- determine how far they can scale.

Read More...

Predictive analytics is moving from personal lines into commercial underwriting. The data challenges are harder, but the potential to improve risk selection and pricing accuracy is substantial.

Read More...

Operational resilience -- the ability to absorb disruptions and maintain critical functions -- has become a board-level topic for financial services firms including P&C insurers.

Read More...

More granular pricing segmentation is generally assumed to improve loss ratios. But there are real limits and tradeoffs that actuaries and pricing leaders must understand.

Read More...

Many insurance carriers that launched ambitious digital transformation programs are experiencing stalled momentum. Understanding the common failure patterns is the first step to getting back on track.

Read More...

Geographic concentration of insured values is a core risk management challenge for P&C carriers. Climate change is increasing the frequency and severity of events that can stress concentrated portfolios.

Read More...

Parametric insurance has proven its value in catastrophe and agricultural contexts. As data infrastructure improves, carriers and MGAs are exploring where else the model can create customer value.

Read More...

Commercial auto has been one of the most challenging P&C lines for several years. Understanding the core loss drivers -- distracted driving, nuclear verdicts, and vehicle repair costs -- is essential for carriers managing this exposure.

Read More...

Insurance faces a well-documented talent shortage as experienced professionals retire and competition for technical skills intensifies. Carriers that invest in development programs are building a durable advantage.

Read More...

Loss control is frequently treated as a regulatory formality in commercial lines. Carriers that elevate it to a genuine value-added service are improving loss ratios and deepening policyholder relationships.

Read More...

Despite growing awareness of flood risk, coverage gaps persist across both the NFIP and private flood markets. Closing those gaps requires product innovation, better risk communication, and distribution reform.

Read More...

Digital distribution tools are reshaping how carriers and independent agents interact. The carriers investing in agent technology are building loyalty -- while those that are not risk losing shelf space.

Read More...

Workers compensation is navigating medical cost inflation, evolving return-to-work practices, and the early adoption of AI for triage and case management. Carriers and employers should understand all three.

Read More...

Real-time data access is giving actuaries the ability to monitor rate adequacy continuously rather than at annual review cycles. The shift has significant implications for pricing agility and competitive positioning.

Read More...

Behavioral economics insights -- nudges, defaults, and framing effects -- are being applied by forward-thinking insurers to improve coverage adequacy, timely payments, and claims reporting behavior.

Read More...

Straight-through claims processing -- where low-complexity claims move from FNOL to payment without human touch -- is a growing priority. Here is how to build it and know when it is working.

Read More...

Reinsurance pricing and capacity constraints set at the January 1 renewals will shape what primary P&C carriers can and cannot offer through 2026. Understanding those dynamics is essential for carrier executives.

Read More...

Cyber insurance pricing and availability have tightened significantly as loss experience has accumulated. Underwriters are demanding more from applicants, and carriers are rethinking their exposure concentrations.

Read More...

In a commoditized personal lines market, customer experience is emerging as a durable differentiator. Carriers that invest in frictionless digital journeys are seeing measurable retention gains.

Read More...

Third-party administrators are no longer just cost centers for claims outsourcing. Strategic TPA partnerships are becoming a source of operational innovation and market access for P&C carriers.

Read More...

Claims fraud costs the insurance industry billions annually. Machine learning models are now identifying suspicious patterns faster and more accurately than traditional rule-based systems.

Read More...

Telematics started in personal auto but is now influencing commercial property, marine, and workers compensation. The underlying shift is carriers learning to use real-time sensor data for risk management.

Read More...

Regulatory activity in insurance is expected to intensify in 2026. Carriers and MGAs that monitor key developments early will be better positioned to adapt with minimal disruption.

Read More...